Analysts often describe investing as a journey, but many investors unknowingly begin that journey with all their resources concentrated in a single asset. Some rely entirely on high-yield bank accounts, others tie up their net worth in illiquid real estate, while some place all their funds into a single equity position. While these approaches may seem straightforward, they expose capital to significant, unhedged risks.

A diversified portfolio mitigates this vulnerability by spreading capital across distinct asset classes that react differently to macroeconomic shifts. Rather than relying on a single vehicle to achieve every financial objective, structural diversification allows investors to balance capital preservation, predictable income generation, structural liquidity, and long-term capital appreciation.

For Kenyan investors, strategic diversification has become paramount amid a shifting interest rate environment, persistent inflationary pressures, and evolving domestic capital markets. Understanding how to construct a resilient portfolio is the first step toward safeguarding wealth through volatile market cycles.

What Diversification Really Means (The Portfolio Variance Framework)

Diversification is the deliberate practice of allocating capital across uncorrelated asset classes, sectors, and investment vehicles to reduce the impact of poor performance from any single holding.

In financial theory, this relies on the concept of correlation; how different assets move in relation to one another. The objective pairs assets with low or negative correlation. When one asset class experiences downward pressure due to macroeconomic headwinds, another remains stable or captures upside, thereby smoothing the portfolio’s overall volatility (the “smoothing effect”).

An Important Distinction: Diversification does not eliminate market risk (systematic risk), which affects the entire economy. Instead, it systematically reduces idiosyncratic risk—the risk specific to a single company, property, or debt issuer.

Ultimately, an optimized portfolio balances four core pillars:

-

Capital Preservation: Protecting the nominal value of core assets.

-

Income Generation: Securing predictable, recurring cash flows.

-

Liquidity Optimization: Ensuring rapid access to cash without incurring penalizing liquidation costs.

-

Capital Growth: Outpacing inflation to grow real wealth over multi-year horizons.

Why Diversification Matters for Kenyan Investors

Navigating the Kenyan macroeconomic landscape requires balancing unique structural opportunities against specific local risks:

-

Inflationary Erosion: Standard savings accounts rarely yield returns that outpace the Consumer Price Index (CPI). When inflation erodes purchasing power, low-yield cash allocations effectively lose real value.

-

Interest Rate Volatility: Fluctuations in Central Bank Rates (CBR) directly impact yields on government securities and commercial bank valuations, making fixed-income timing a critical variable.

-

The Real Estate Liquidity Trap: While local investors highly favor property investment, real estate remains fundamentally illiquid. Liquidating a physical asset during a market downturn can take months or years, often forcing steep price concessions if the owner requires cash urgently.

By diversifying, an investor avoids becoming hostage to a single asset class’s cyclical downturn. If equities face a bearish cycle on the Nairobi Securities Exchange (NSE), an optimized allocation in short-term debt instruments or fixed-income funds can anchor the portfolio’s overall yield.

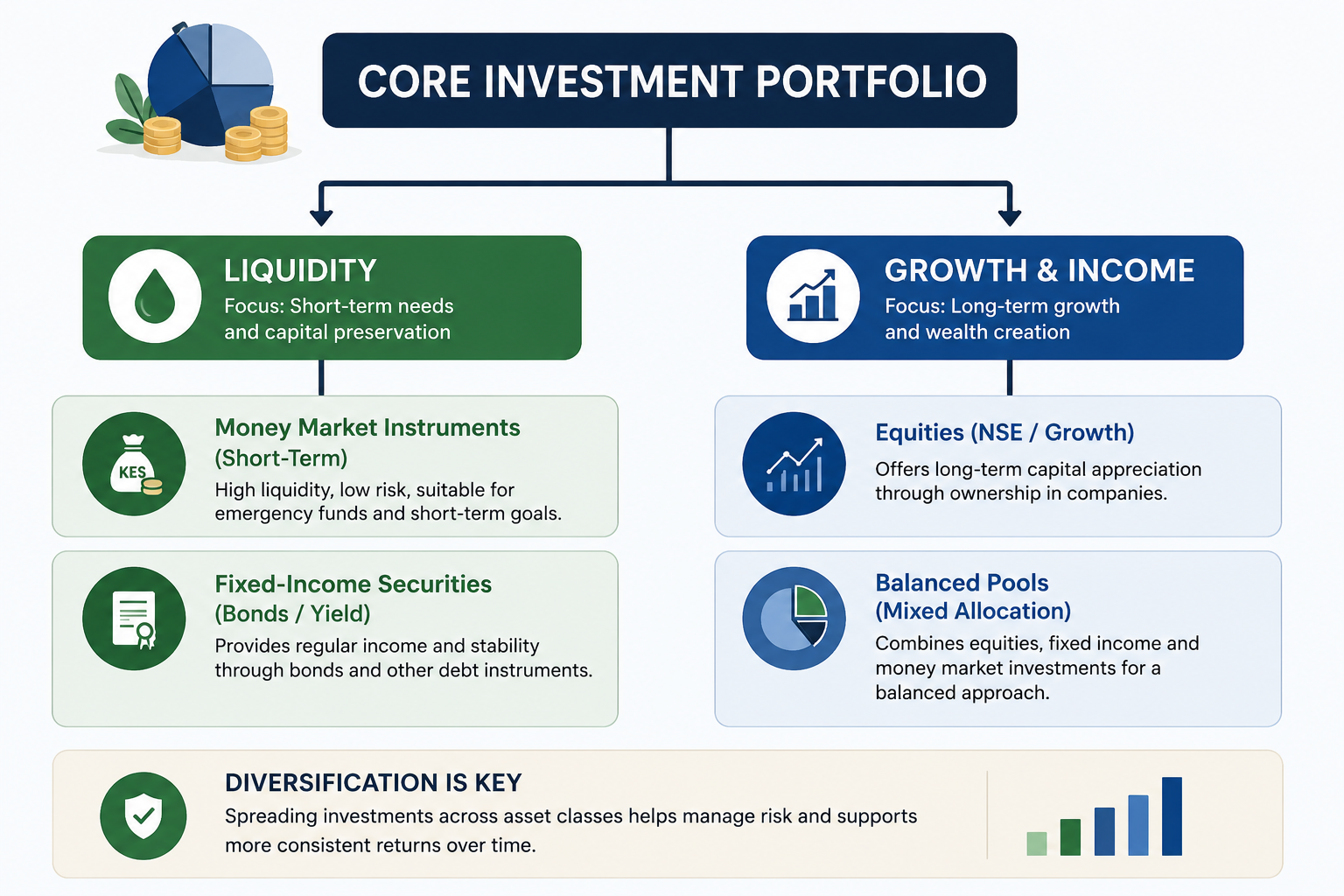

The Four Building Blocks of a Kenyan Diversified Portfolio

1. Cash and Liquidity Instruments

Liquidity represents tactical flexibility. Investors require seamless access to capital for emergency reserves, short-term liabilities, or sudden, mispriced market opportunities.

Money Market Instruments—such as Treasury Bills (T-Bills) and high-quality commercial paper—allow investors to maintain high liquidity while earning compounding returns that typically outperform traditional banking accounts.

2. Fixed-Income Securities

Fixed-income allocations focus on mitigating capital volatility while providing structured, predictable cash flow.

This category comprises Treasury Bonds (T-Bonds), infrastructure bonds, corporate debt obligations, and managed fixed-income pools. Because debt issuers must legally prioritize interest payments over equity dividends, these instruments provide a vital stabilizing counterweight when broader markets experience turbulence.

3. Equities

Equities represent fractional ownership in businesses and serve as the primary engine for long-term compounding and wealth creation.

While listed shares experience short-term price volatility driven by market sentiment and corporate earnings cycles, they offer unique access to capital appreciation and dividend income. For long-term horizons, an equity allocation is essential to combat the compounding effects of inflation.

4. Balanced Strategies

Balanced allocations combine equities, fixed income, and liquidity instruments within a single, structurally managed vehicle. This approach automates diversification, making it highly effective for investors who prefer a holistic, professionally rebalanced exposure to managing separate asset silos.

Sample Allocations Across Risk Profiles

Investors should never allocate assets arbitrarily. Specific time horizons, liquidity requirements, and an individual’s psychological capacity for risk must dictate the strategy.

The following models illustrate how an investor can structure a portfolio within the Kenyan investment framework:

Conservative Model

Optimized for wealth preservation, immediate income, and risk aversion.

| Asset Class |

Target Allocation |

Primary Objective |

| Money Market Instruments |

60% |

Immediate Liquidity & Principal Stability |

| Fixed-Income Securities |

30% |

Predictable Yield Generation |

| Equities |

10% |

Minimal Inflation Hedge |

Moderate Model

Optimized for a balanced mix of current income and long-term capital growth.

| Asset Class |

Target Allocation |

Primary Objective |

| Money Market Instruments |

25% |

Tactical Liquidity Reserve |

| Fixed-Income Securities |

35% |

Core Income Anchoring |

| Equities |

25% |

Growth Capital Exposure |

| Balanced Strategies |

15% |

Managed Multi-Asset Diversification |

Growth-Oriented Model

Optimized for maximum capital appreciation over an extended time horizon ($>5$ years).

| Asset Class |

Target Allocation |

Primary Objective |

| Money Market Instruments |

10% |

Baseline Emergency Cash |

| Fixed-Income Securities |

20% |

Portfolio Stabilization |

| Equities |

55% |

Aggressive Capital Compounding |

| Balanced Strategies |

15% |

Opportunistic Asset Allocation |

Pitfalls in Portfolio Diversification

True diversification requires deliberate, analytical construction. Many investors fall victim to structural blind spots:

-

The Illusion of Diversification (Naïve Diversification): Buying shares in five different commercial banks listed on the NSE does not constitute diversification; it creates sector concentration. If the financial sector faces regulatory changes or credit shocks, the entire selection will decline simultaneously.

-

Ignoring the Real Return Equation: Evaluating performance purely on nominal yield carries significant risk. If a portfolio generates a nominal return of 10% in an environment where inflation sits at 6%, the true expansion of wealth—the Real Return—is approximately 4%:

-

The High Yield Trap (Chasing Past Returns): Reallocating capital entirely into whichever specific asset outperformed the market last quarter often results in buying at cyclical peaks, exposing the portfolio to severe corrections.

-

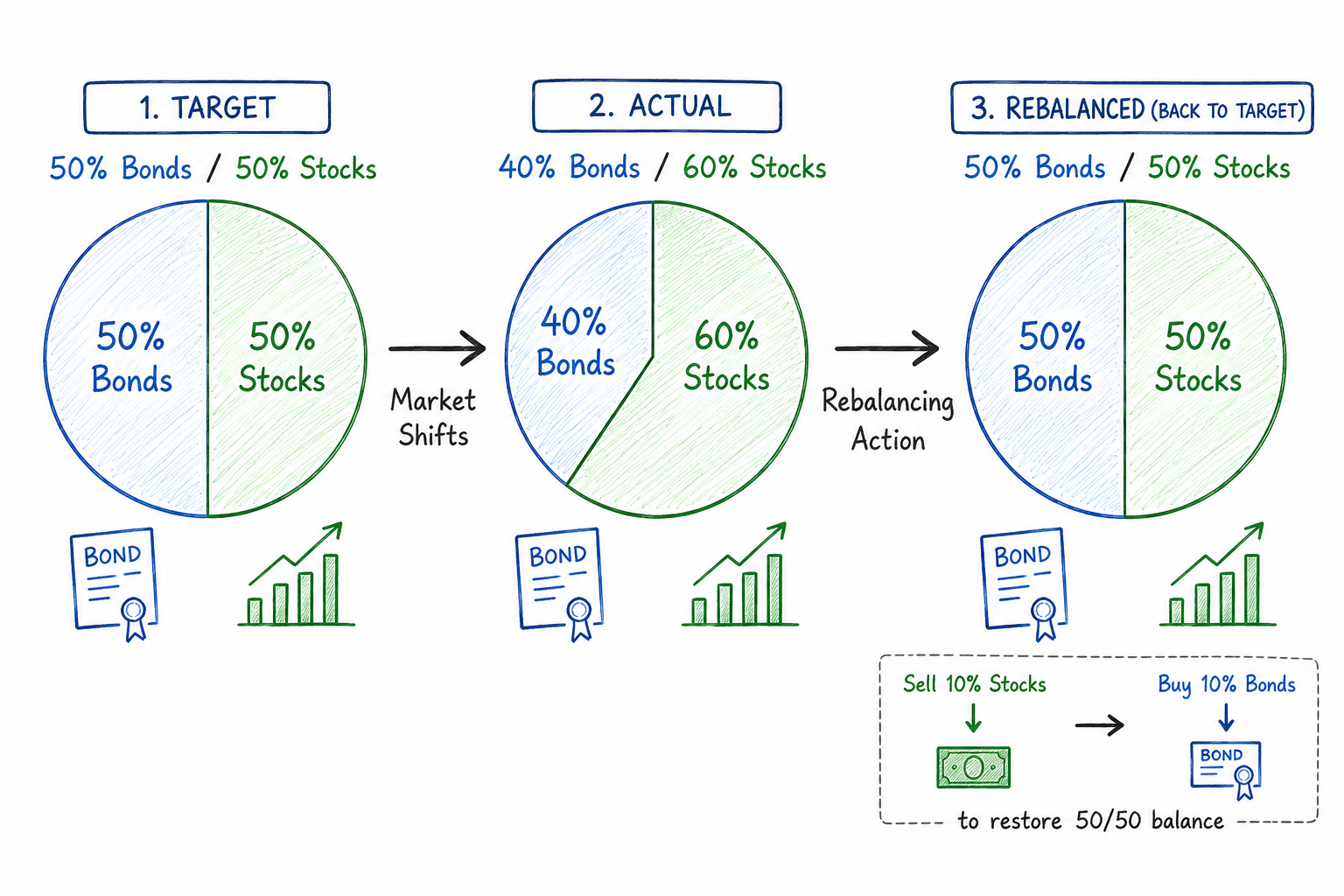

Neglecting Rebalancing Protocols: Over time, a strong equity market will increase the relative weight of shares in a portfolio, inadvertently shifting a Moderate profile into a Growth profile without the investor’s explicit consent.

Portfolio Optimization: The Rebalancing Discipline

Diversification is a dynamic process, not a static product. As different underlying assets grow at variance, your actual asset allocation drifts away from your target strategy.

Portfolio rebalancing is the systematic process of selling a portion of overperforming, overweighted assets and deploying that capital into underperforming, underweighted assets.

- The Frequency: Investors should review allocations systematically—typically annually or semi-annually—or when a major life milestone changes their fundamental risk capacity.

- The Benefit: It enforces an unemotional, disciplined buy-low/sell-high mechanism, preventing emotional bias from dictating portfolio adjustments during market highs or lows.

Structuring Portfolios Around Distinct Financial Milestones

An effective strategy constructs portfolios backward from clearly defined financial liabilities, rather than forward from investment products.

Emergency Reserves

-

Horizon: Immediate (0-12 Months)

-

Strategy: The planner places priority entirely on liquidity and absolute capital preservation, heavily weighting assets toward money market allocations.

Education Planning

-

Horizon: Medium to Long-Term (3-10 Years)

-

Strategy: This goals-based approach employs a blended framework. Early years lean heavily toward equity growth to match rising tuition inflation, before transitioning into high-yield fixed income as graduation timelines approach.

Retirement Wealth Accumulation

-

Horizon: Long-Term (10+ Years)

-

Strategy: This structure maximizes allocation to compounding growth engines like equities and balanced vehicles during the accumulation phase, progressively transitioning to capital preservation and cash flow generation as retirement nears.

Beyond Complexity: The Power of Streamlined Allocation

True diversification does not mean over-complicating a portfolio with dozens of fragmented holdings. Instead, it means selecting a cohesive matrix of complementary asset classes that work collectively to protect capital, generate yield, and build sustainable, long-term purchasing power.

For Kenyan investors looking to insulate their wealth from market volatility, deliberate asset allocation remains the most dependable mechanism for achieving enduring financial independence.

Frequently Asked Questions

What is a diversified investment portfolio?

It is an investment strategy that distributes capital across distinct, uncorrelated asset categories (such as cash equivalents, fixed-income instruments, and equities) to mitigate the risk of severe capital loss from any single underperforming asset.

How much capital do I need to start diversifying in Kenya?

Modern investment options have removed the old barriers to entry. Collective investment schemes (CIS) and pooled funds allow retail investors to access professionally managed, diversified underlying portfolios of T-Bills, bonds, or equities with highly accessible initial deposits.

Can diversification eliminate investment risk?

No. Diversification eliminates unsystematic (asset-specific) risk, but it cannot protect against systematic (market-wide) risks such as global recessions, currency depreciations, or broad macroeconomic shocks.

How often should I analyze my portfolio?

You should conduct a comprehensive portfolio audit and rebalancing review at least once a year, or whenever your personal risk tolerance or investment horizon undergoes a material change.

Is a diversified approach suitable for novice investors?

Yes. Diversification is a foundational tenet of prudent wealth management. It protects beginner investors from the high-impact mistakes often associated with speculative asset concentration.